Independence in music is no longer defined chiefly by aesthetic posture or outsider identity. In 2026 it is increasingly measured by the operational infrastructure artists and labels are able, or unable, to build around ownership, data, direct relationships, and economic control. This editorial examines what real autonomy requires when scale, consolidation, and platform logic continue to reshape the field.

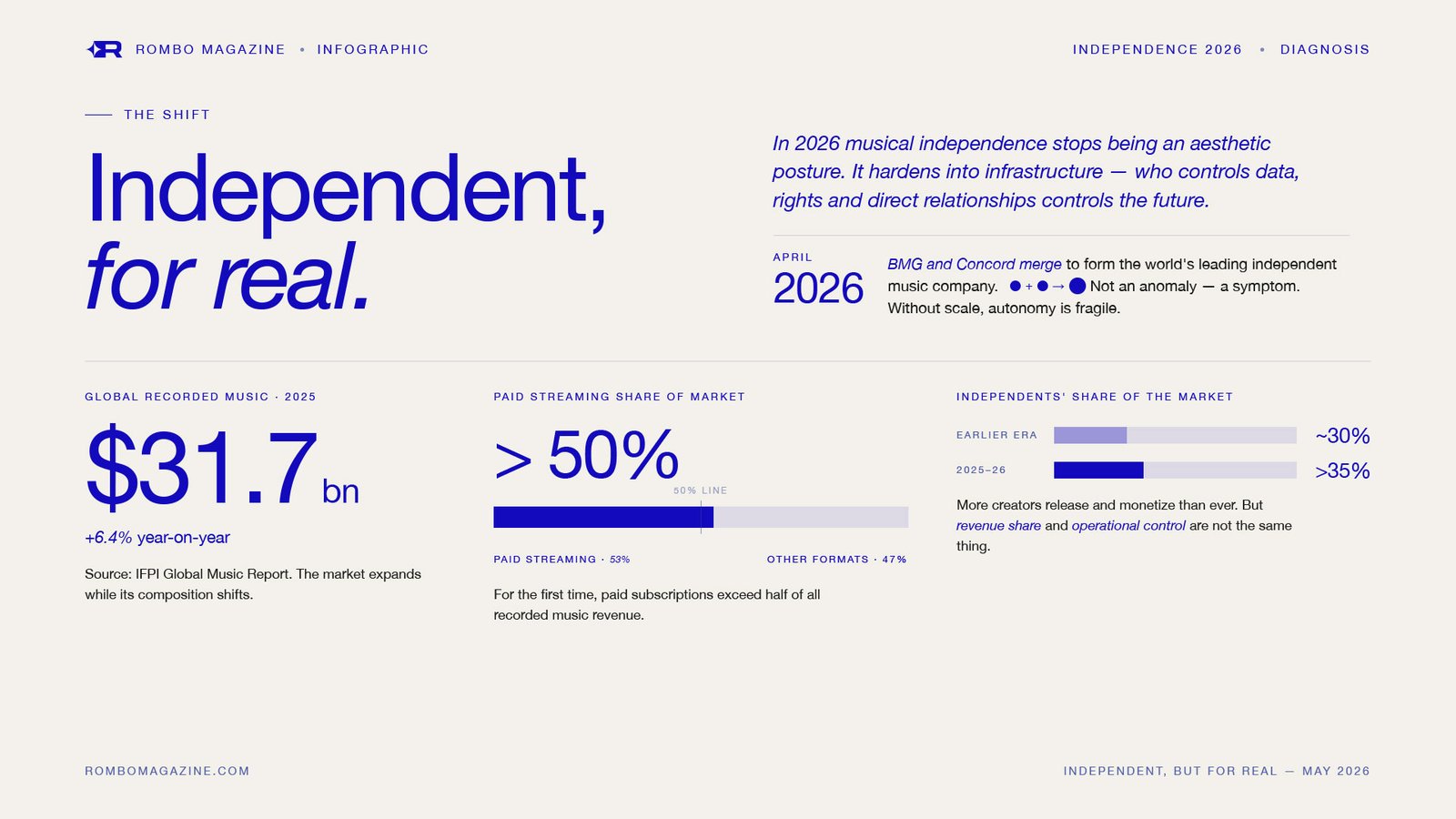

The April 2026 announcement that BMG and Concord would combine to form the world’s leading independent music company was not an anomaly. It was a symptom. Musical independence is no longer primarily a question of sonic sensibility, outsider posture, or label identity. It is hardening into a question of infrastructure: who controls the systems that turn sound into reach, revenue, and durable careers.

When two substantial “independent” entities merge to create something with the resources and global footprint of a near-major, the old framing starts to feel incomplete. The combined company, operating under the BMG name with divisions for publishing and recorded music, is explicitly positioned as the leading independent player. Yet its scale, ownership structure, and capacity for investment in technology and talent sit far beyond what most independent operations can muster. This is not a betrayal of independence. It is evidence that meaningful independence in a platform-dominated, capital-intensive market increasingly demands structural weight.

The move reflects a broader calculation: autonomy without leverage is fragile. In distribution, rights administration, data infrastructure, and international reach, size has become a form of protection. Smaller operations that once defined themselves against corporate scale are now forced to ask whether romantic notions of independence can survive without comparable tools.

Global recorded music revenues reached $31.7 billion in 2025, up 6.4 percent, with paid streaming accounting for more than half of the total for the first time. Within this expanding market, independent artists and labels have captured a growing share — broadly estimated in the high thirties percent range and rising from earlier levels around 30 percent. More creators can release, monetize, and reach audiences than at any previous point in the streaming era.

Yet revenue share and operational control are not the same thing. Many of the tools that convert releases into visibility and sustained income, sophisticated distribution networks, playlist access, marketing technology, and rights management platforms — sit within or adjacent to larger corporate structures. Algorithmic discovery remains heavily influenced by scale and existing catalog power. The result is a landscape in which more music circulates, but the conditions under which it circulates are still shaped by concentrated infrastructure.

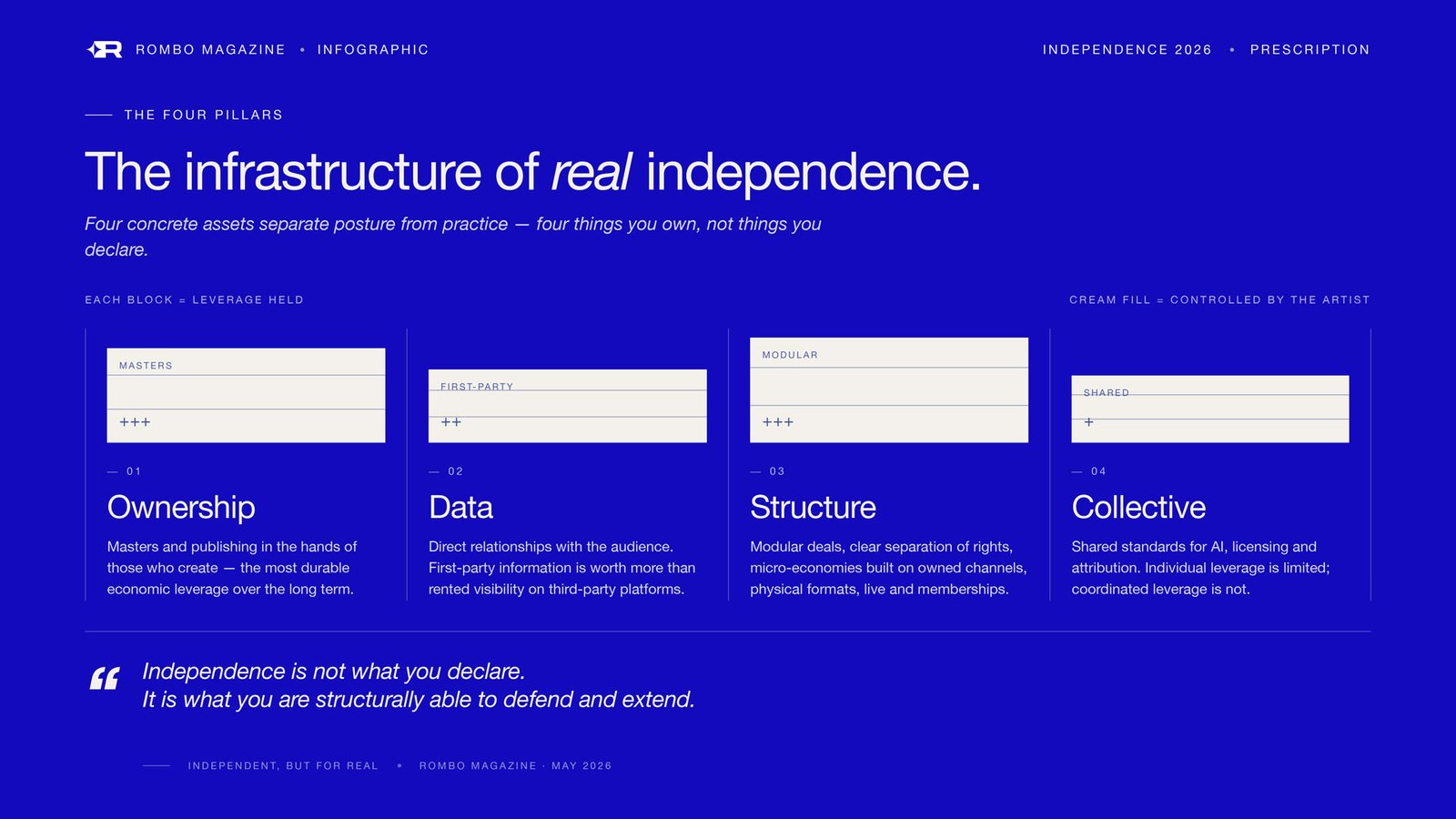

At the level of individual artists and smaller labels, the operative meaning of independence has shifted toward ownership of concrete assets. Data, particularly direct fan relationships and first-party information — has become more valuable than rented visibility on third-party platforms. Micro-economies built around owned channels, physical formats, memberships, and targeted live activity offer a measure of insulation from algorithmic volatility.

This is not a return to pure DIY isolation. It is a recognition that independence functions best when it includes control over the economics and information that surround the work. Modular deal structures, clearer separation of rights, and deliberate investment in direct-to-fan infrastructure are practical expressions of this shift. Artists and labels that treat their careers as systems to be engineered, rather than releases to be promoted, are building different kinds of durability.

The integration of AI into recommendation, production, and licensing layers introduces new dependencies. Training data, attribution standards, and licensing terms are infrastructure questions as much as they are creative ones. Independent publishers and label groups have begun exploring collective positions precisely because individual leverage is limited. Without coordinated standards for rights clarity and fair participation in emerging systems, even successful independent work risks subsidizing platforms and models over which creators have little say.

Platform fatigue is real. So is the premium on human context, storytelling, and verifiable provenance. The independents positioned to benefit are those investing in the technical and relational infrastructure that lets them operate with greater intentionality — whether through owned channels, ethical technology partnerships, or shared bargaining frameworks.

Independence retains its critical and cultural force when it functions as infrastructure for autonomy rather than as a stylistic or attitudinal category. The distinction matters. An aesthetic of independence can be adopted without changing underlying power relations. Operational independence, ownership of masters and publishing where possible, control of data and direct relationships, participation in standards that protect creators, produces different outcomes over time.

The artists, labels, and publishers who understand this are not necessarily the loudest or the most visible in any given week. They are the ones building or securing the systems that let music exist on terms they have helped shape. In 2026, that is the measure that separates posture from practice. Independence is not what you declare. It is what you are structurally able to defend and extend.